Ultimately, you want to surround yourself with multiple streams of income. We love speculation because it offers us a chance to leapfrog our net worth higher, but always remember to take those profits and turn a good portion into sustainable income.

In a zero interest-rate environment, investors have become starved for reliable income.

Many have mistakenly chosen to turn to Wall Street for their answer, but with stocks that are already at all-time highs, investors looking for income may soon find themselves on a roller coaster ride with their principal investment. Using your capital to either compound your wealth or live off of the income your dollars can generate should be a chief objective for anyone seeking financial independence.

Here are my top 5 income strategies that are outside the realm of Wall Street.

1. PeerStreet:

I am more impressed with this company than any other I’ve interacted with. First of all, Brett Crosby, one of the founders, is the guy who created Google Analytics. This is a brilliant team of entrepreneurs who are trying to disrupt the entire mortgage industry.

A key investor in the company is Dr. Michael Burry. He was the star of the movie The Big Short, played by the actor Christian Bale. You can help crowdfund a short-term mortgage, 3 to 5 years, at interest rates of 7 to 9%. You can also choose to set a conservative loan-to-value below 70%, offering up plenty of equity in case of foreclosure.

PeerStreet handles it all, of course. All you have to do is choose how much you want to participate in each mortgage that comes available.

The minimum investment amount is $1,000. I’ve personally kept it between $2,000 and $5,000 in order to diversify my holdings nationwide and limit my risk in a worst-case scenario situation.

Of the 106 loans I’ve participated in, 24 have been paid off, 1 is late and being contacted for payment, and 81 are making their mortgage payments monthly, giving me a yield of about 7.5%.

This is a very passive way to invest for cash flow, and I have to admit that I prefer PeerStreet because it is backed by the single-family home.

2. Ceres Farms:

Ceres allows investors to participate directly in a diversified portfolio of farmland that offers current income, capital appreciation, an inflation hedge, and favorable diversification that is negatively correlated with traditional asset classes.

Ceres has assets of $620 million, which consists of more than 100,000 acres of prime U.S. farmland.

Farmland acquired by the fund is effectively owned by each investor, proportional to their investment in the fund. Ceres then leases the land to its expanding network of farmers, currently consisting of 55 production teams in 10 states, who either pay cash for rent or 40% of gross revenue.

These farm operators view Ceres as their partner who acquires the additional tillable acres that they all desperately need to grow so that they can improve their efficiency and profits.

It’s another hard-asset-backed income producer!

3. Lending Club: It’s Peer-to-Peer Lending

We do NOT recommend Lending Club the stock. However, as investors making loans, I have personally been a satisfied client for the past year. My experience has been an adjusted net annualized return of 11.57%, by making small loans to consumers. Most are to refinance current debt, some are to start businesses, and others are to purchase goods and services.

The average borrower makes over $75,000 per year, has a credit score of over 660, and has a 2-year job history. No doubt, this can be risky, as with all lending, but like any creditor, over time, lending money can be very profitable.

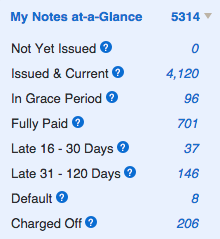

I have currently made 5,314 loans that I’ve funded, and as you can see, not all of them have performed, but the ones that have have more than recovered any losses experienced on the very small percentage that default.

To become an investor in Lending Club is easy. Simply go to LendingClub.com and go through the steps. I would suggest starting off real small since you are committing your capital for at least 3 years.

You can choose to reinvest interest payments into new loans or receive a monthly check. Because I am young and I’m looking to compound my savings, I have opted to reinvest into new loans, but if you’re looking for a reasonably reliable income, you can request to have your interest payments electronically transferred into your personal bank account.

4: The Single-Family Home

I’ve had a horrible to just an okay experience with multi-family units, like duplexes and a 4-plex. The cash flow has been very volatile for larger units, and the quality of renter has also not been nearly as good as the homes I have purchased for the past 18 years.

With that said, for rental income, stick with single-family homes in nice middle-class neighborhoods. Only buy homes that cash-flow, which means you may have to look out of state or within a few hours’ drive from your own residence.

My wife and I personally have a single-family home that we’ve owned for over 10 years, and we’ve never seen it! We haven’t even traveled to the state the property is located in, completely relying on the people we hired to manage it.

When it comes to buying rental property, have an open mind when seeking cash flow. Many investors can’t find good deals in their own area, so they write this idea off completely, but that’s a terrible mistake. I can’t think of a safer, more stable way to receive reliable income than from a middle-class family that is looking to rent a house.

After buying a property that cash-flows, treat your tenants the same way the Marriott treats their occupants: over-deliver..

Make sure the property is clean, in good working order, and when they do have an issue, be quick to resolve it. Also, when holidays come around, be sure to send your tenants a gift and let them know you appreciate them.

Basically, treat your rental property like a business, because it is, and treat your tenants as clients, because they are!

5: Whole Life Insurance

For a compounded savings and a place to store your wealth, I don’t think you can beat this idea.

If you want life insurance, then buy term, but if you’re looking to grow your wealth and have it protected — even from the IRS — use whole life insurance as a vehicle to compound and protect your savings.

The knowledge of benefits and education that is needed in order to take part in this exceptional income compounding strategy is deeper than any other idea the financial industry will ever offer you. I suggest for those of you interested to start with the book Bank on Yourself, by Pamela Yellen.

It takes a specialized agent to even set one of these up properly, because you’re not interested in the life insurance at all, you’re simply using the tax code and the insurance as a vehicle to grow your wealth.

Feel free to contact my personal agent, Jennie Steed, at Paradigm Life, but please take the time to educate yourself on this prior to going down this route, because once you understand it, you’ll be able to benefit from this powerful tool.

Summary: we are surrounded by income ideas, and each week in November, I will be sharing with you some of my favorite new ideas for cash flow.

Imagine if nearly all your investments went into ideas that produced income… where would you be in 10 years from now, or 15 or 20 years?

Investing for cash flow is the single greatest financial discipline you can have over the course of your lifetime.

True wealth and financial security come from having multiple streams of income.

Best Regards,

![]()

Daniel Ameduri

President, FutureMoneyTrends.com